Summary

Building on the industry selection framework from Part I and the venture debt analysis in Part II, this essay asks the equity question: can AI-powered roll-ups realistically deliver a 10x return for venture investors?

To answer this, a financial model was built to simulate how an AI roll-up could compound over ten years across multiple acquisition cycles and financing rounds. The short answer is yes—but conditions apply.

Download the model and run your own assumptions: AI Roll-up Financial Model (Google Sheets)

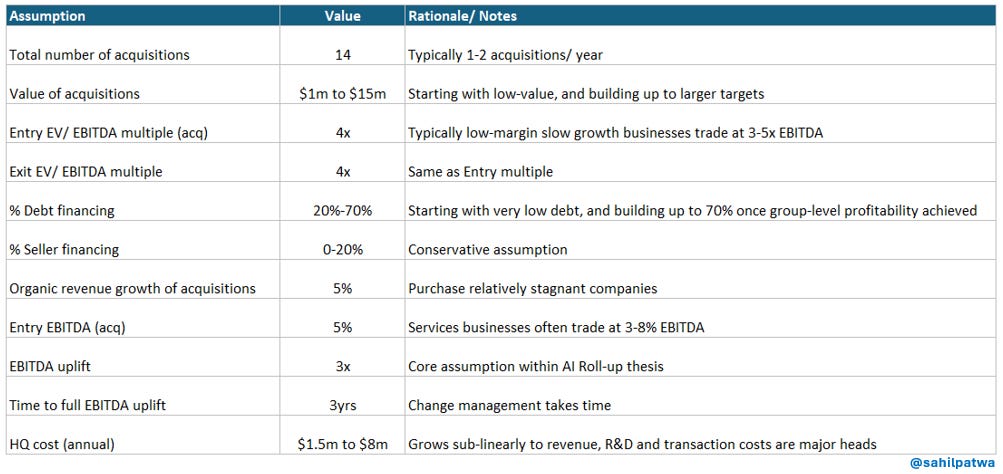

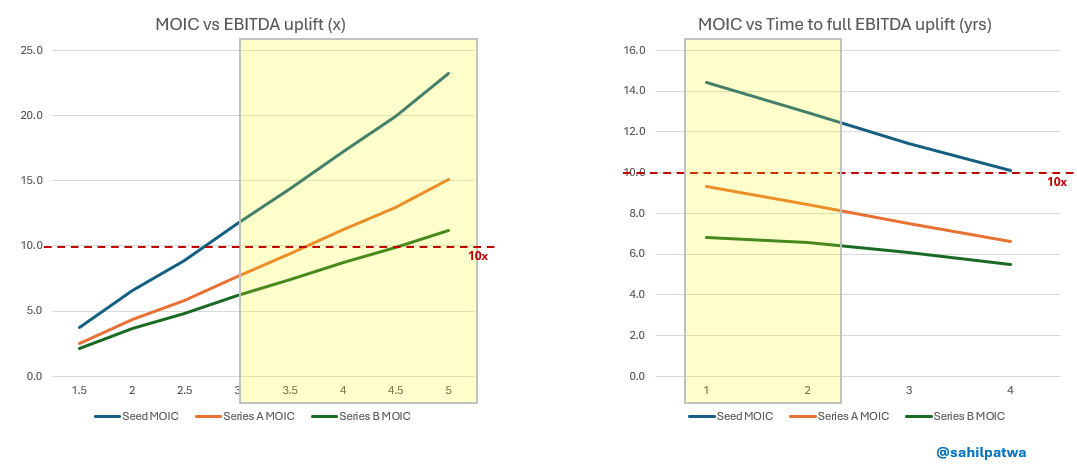

In a base-case scenario—acquiring companies at modest multiples and applying AI to drive meaningful EBITDA improvement—an AI roll-up can reach $500M+ ARR and ~$70M EBITDA within ten years, with less than $50M in total equity raised. That math creates a genuine 10x path for Seed investors, though returns compress at later stages.

Five Conditions for 10x Returns

1. A credible path to 4–5x EBITDA uplift. This is the most critical lever. Even a 2–4x uplift produces a compelling business—but 4x+ is nearly essential for Seed-stage 10x outcomes. Critically, speed matters: faster uplifts free up cash for reinvestment sooner, amplifying compounding.

2. Fewer equity rounds, but with higher dilution per round. Plan for 3–4 financing rounds total. Once early acquisitions are generating cash, debt and seller financing should carry the load. Expect 25–30% dilution per round—higher than typical VC deals, but still leaving founders 30–50% equity at exit.

3. HQ costs that scale sub-linearly. Lean central overhead is essential, especially early when capital must stretch across both R&D and acquisitions. Bloated HQ costs erode the efficiency gains that make this strategy work.

4. A founding team with combined industry, tech, and M&A expertise. Strong founder profiles unlock larger seed rounds and earlier access to venture debt, both of which meaningfully improve return profiles.

5. No reliance on multiple expansion. Models that assume an exit at 10–12x EV/EBITDA when acquisitions were made at 3–4x are fragile. Build the case on operational improvement alone—multiple expansion, if it comes, is a bonus.

When these conditions are met, AI roll-ups can offer genuine venture-scale returns—making them one of the few models that combine PE-style cash flow predictability with VC-style upside.