It's not a stretch to say that debt will likely account for at least half of the total capital raised by most AI Roll-ups over their lifetime. As a corollary, being thoughtful about how you raise that debt is critical. Yet, it's also the topic that the majority of founders I've spoken to are least comfortable with.

A few months ago, we hosted a credit masterclass with Linus from TechCredit Partners for a small group of 25 AI Roll-up founders, and the response was phenomenal. Still, the questions kept coming. No clear founder-friendly guide to raising debt for AI Roll-ups exists right now, so I asked Linus to co-author this with me. Together, we'll unpack what you can expect when raising debt for your AI Roll-up - the key concepts, lender psychology, and the trade-offs that actually matter.

We expect this guide to be especially helpful for founders navigating the debt raising journey for the first time.

Before we dive in, one of Linus's favorite quotes sets the tone perfectly:

"Venture capital is all about making a possible $100 from $1, while debt is about making a certain $1 from $100."

It's a simple but powerful framing, and an excellent lens for understanding how lenders think.

Contents

- 1. Debt: Basic Terms and Concepts

- 2. Debt Instruments Commonly Used in AI Roll-ups

- 3. Who Are the Players

- 4. What Lenders Really Look For

- 5. Key Elements to Consider When Choosing a Lender

- 6. Debt Capacity Benchmarks

- 7. Timeline & Process

- 8. The Real Price-tag of a Debt Raise

- Appendix A: Term Sheet Bingo

- Appendix B: Watchouts and Horror Stories

- Appendix C: FAQs

1. Debt: Basic Terms and Concepts

The credit world loves complexity. You'll find structures for every imaginable scenario, but in practice, three concepts matter most when you're starting out: how interest is repaid, how principal is repaid, how the debt is secured, and how the debt will help you to generate overall equity value. Mastering these gives you a good foundation for navigating most debt discussions.

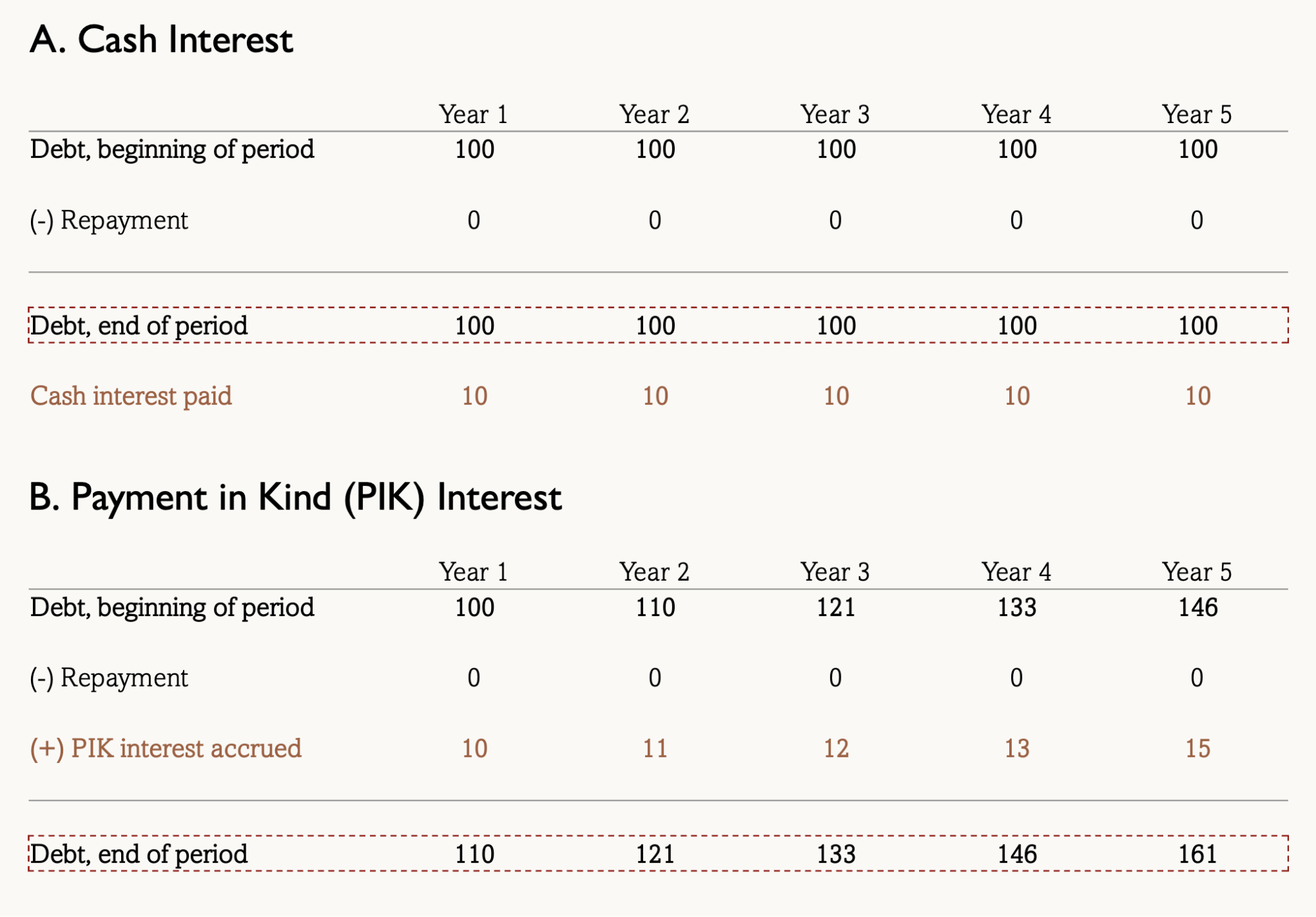

1a. Mechanisms for Interest Repayment - Cash Interest or PIK?

Cash interest is the portion of a loan's interest that is paid in regular cash installments during the life of the loan, typically monthly or quarterly.

PIK (Payment-in-Kind) interest is interest that is not paid in cash but instead added to the loan balance, increasing the principal owed over time.

For the same principal and interest rate, PIK structures allow you to carry more debt since no immediate cash payments are required. In practice, this is a bit more nuanced: lenders still care about total leverage, not just cashflow. And PIK interest is also usually more expensive than cash interest.

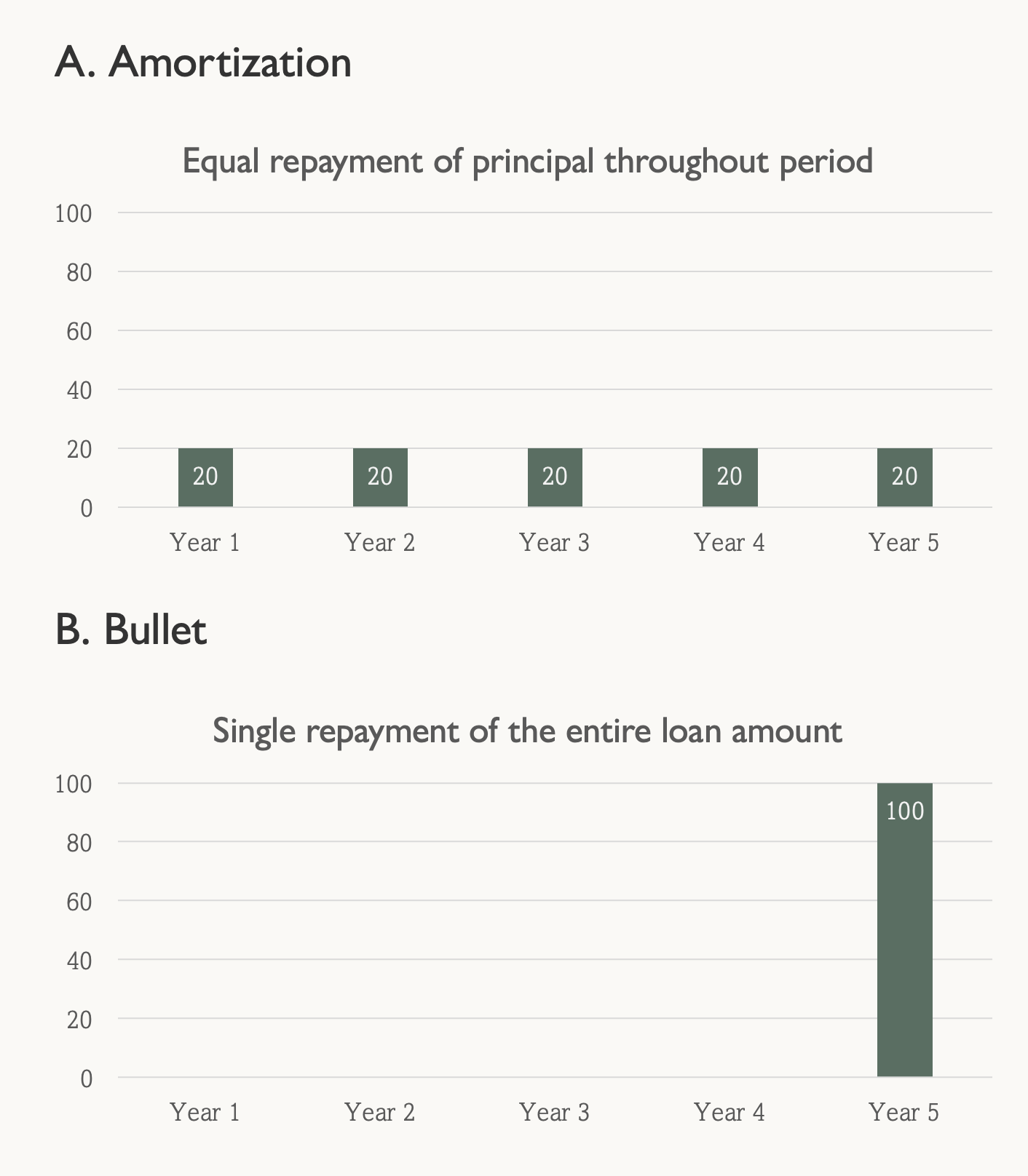

1b. Mechanisms for Principal Repayment - Amortization or Bullet?

Amortization of principal means repaying the loan in regular installments that include both interest and principal, reducing the outstanding balance over time.

Bullet repayment means paying off the entire principal amount in a single lump sum at the end of the loan term.

While the above is a simplistic representation, it is common in amortizing loans to have an interest-only period, during which the borrower pays only interest, allowing time to deploy capital and generate returns before starting principal repayments.

Typically, when maximizing debt capacity or preserving cash flow is key (as in acquisition-driven or growth-heavy roll-ups), Bullet repayments and PIK interest are preferred structures. Though they often come with higher cost and lender scrutiny, and are not always compatible with all lender types (more on that in the next section).

1c. Equity Value Generation

Debt is often described as non-dilutive capital because, unlike issuing equity, lenders do not typically receive ownership upfront. However, certain debt structures can still affect equity value directly or indirectly depending on their terms.

Some debt agreements include equity-linked features that compensate lenders for taking additional risk, particularly in venture debt, growth debt, or higher-risk structured financings. These commonly include:

- Warrants: options granted to the lender that allow them to purchase a small portion of equity at a pre-agreed price, usually exercisable upon an exit or IPO.

- Conversion Features: provisions allowing part of the debt to convert into equity under specific conditions, such as a future financing round, refinancing, or default event.

- Profit Participation Rights (less common): rights that entitle lenders to share in future profits or liquidity proceeds without direct equity ownership.

Depending on the instrument, dilution may range from zero in pure debt structures to approximately 5% in many venture debt facilities, and in more specialized or higher-risk structures, can reach 15–20%.

At the same time, debt affects equity value beyond explicit dilution. Interest rates, amortization schedules, covenants, collateral requirements, and repayment timing all influence how much capital remains available to reinvest in growth versus servicing obligations. Two debt facilities with similar pricing can therefore produce very different outcomes for equity holders depending on how they interact with the company's growth profile and operating model.

The most effective debt solution is not simply the cheapest capital, but the structure that extends runway, preserves strategic flexibility, and allows management to deploy capital into initiatives that increase long-term enterprise value.

It is also worth remembering that your first debt structure is rarely your last. As your roll-up scales and your track record matures, refinancing into larger, cheaper, or more flexible facilities becomes not just possible but expected. The goal early on is to get the right structure for where you are today, one that gives you enough runway and flexibility to prove the model. Better terms will follow.

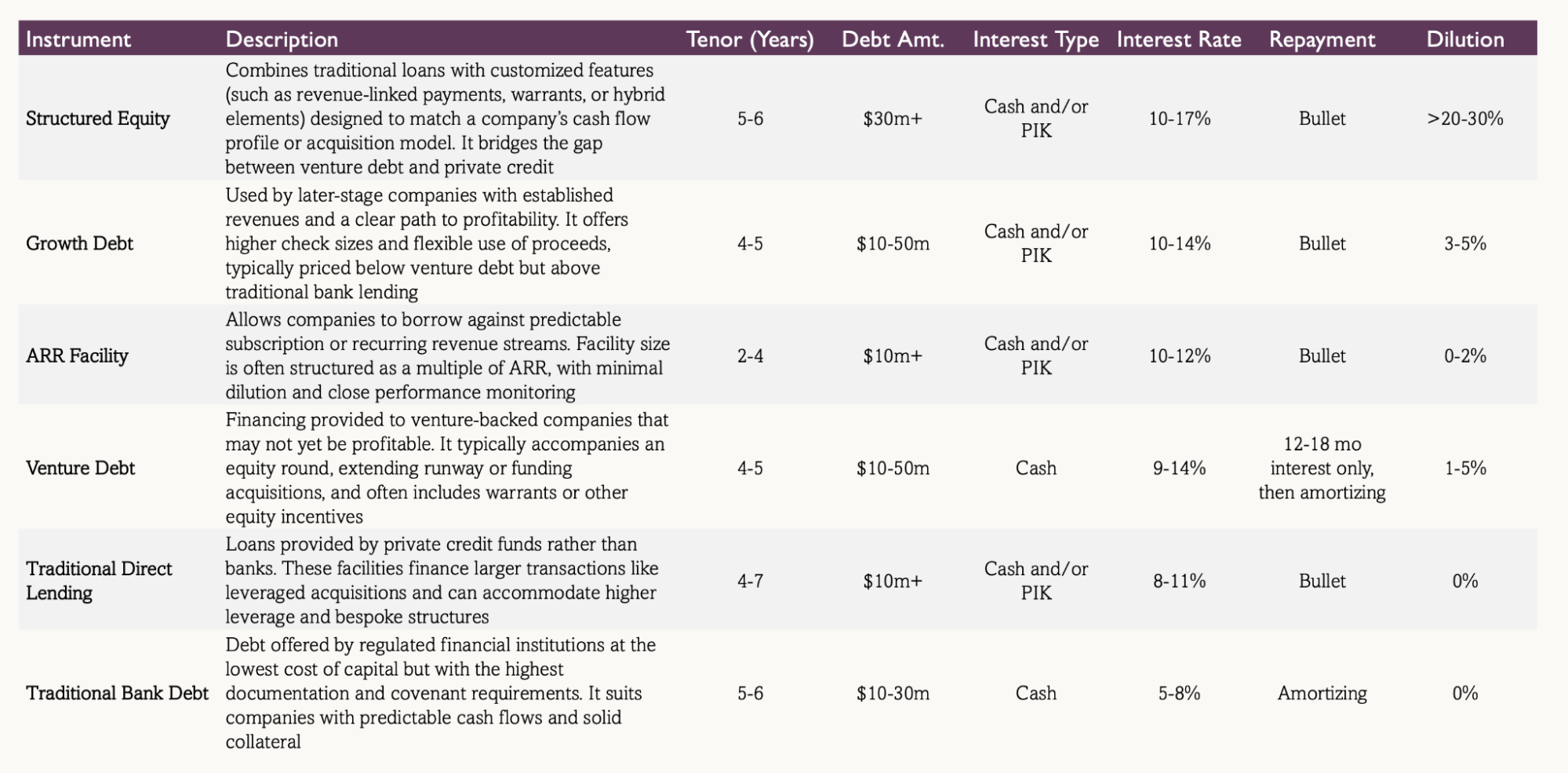

2. Debt Instruments Commonly Used in AI Roll-ups

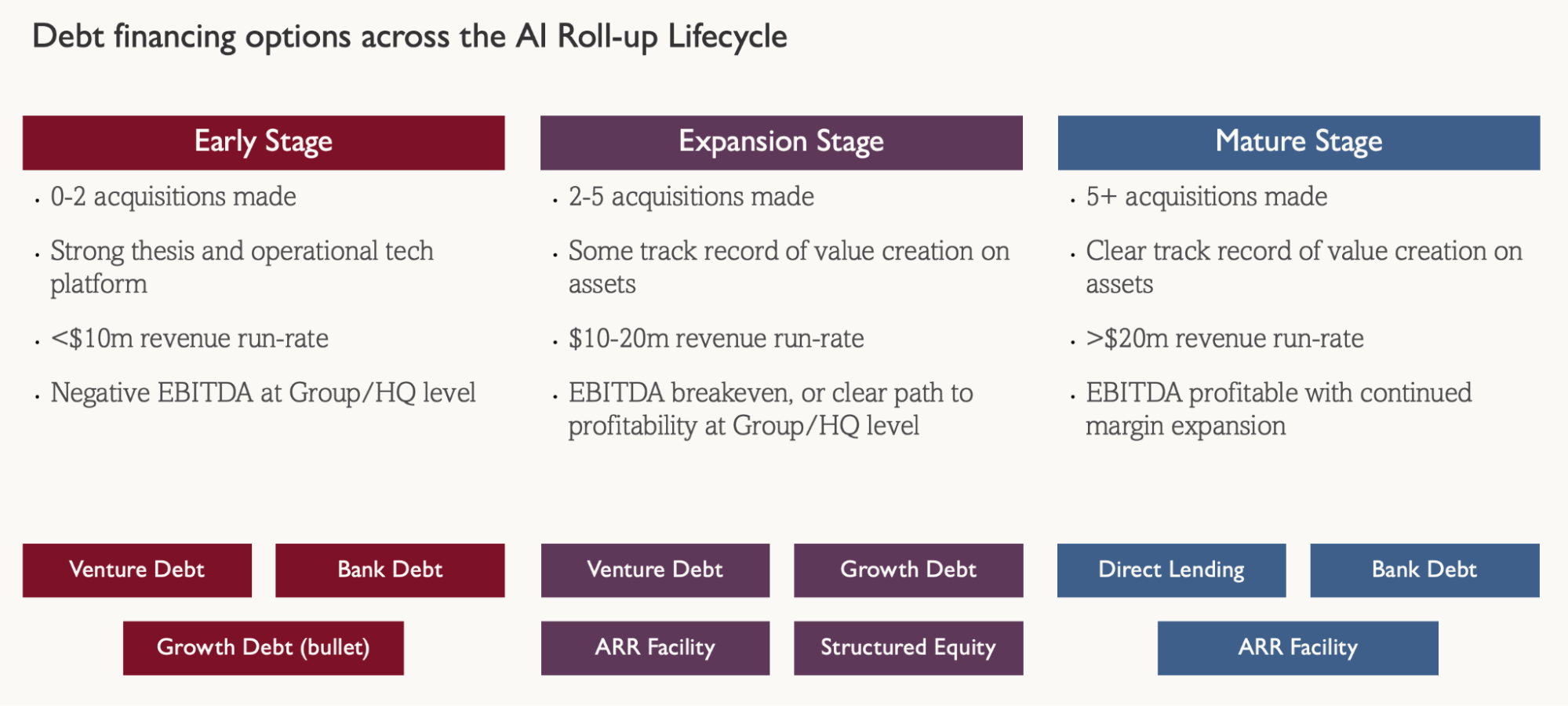

As an AI Roll-up progresses through its lifecycle, both its risk profile and financing needs evolve - and different debt instruments become suitable at each stage. The chart below outlines the most common instruments used by AI Roll-ups and their key characteristics.

AI Roll-ups will be able to unlock different types of debt at different lifecycle stages. This is what a typical progression looks like (even though, every journey is different. For e.g. AI Roll-ups typically hit positive EBITDA much sooner in the journey!):

But what about your first acquisition?

For the first acquisition, most AI roll-ups should predominantly rely on equity and seller notes or earnouts rather than pull in outside debt. Early on, you should prioritize flexibility to iterate on AI transformation and change management to create a transformation playbook, rather than navigating debt covenants.

This shifts if you already have real conviction on cashflows - for example if you have tested the product and validated margin uplift with design partners. Another exception could be when the minimum viable acquisition size is large, say above $10m in enterprise value, and you want to limit the initial equity hit. But if you do not yet have proof points, expect more rigorous scrutiny on your assumptions, and potentially less favourable terms. Make sure any debt you take is an accelerator, not a drag.

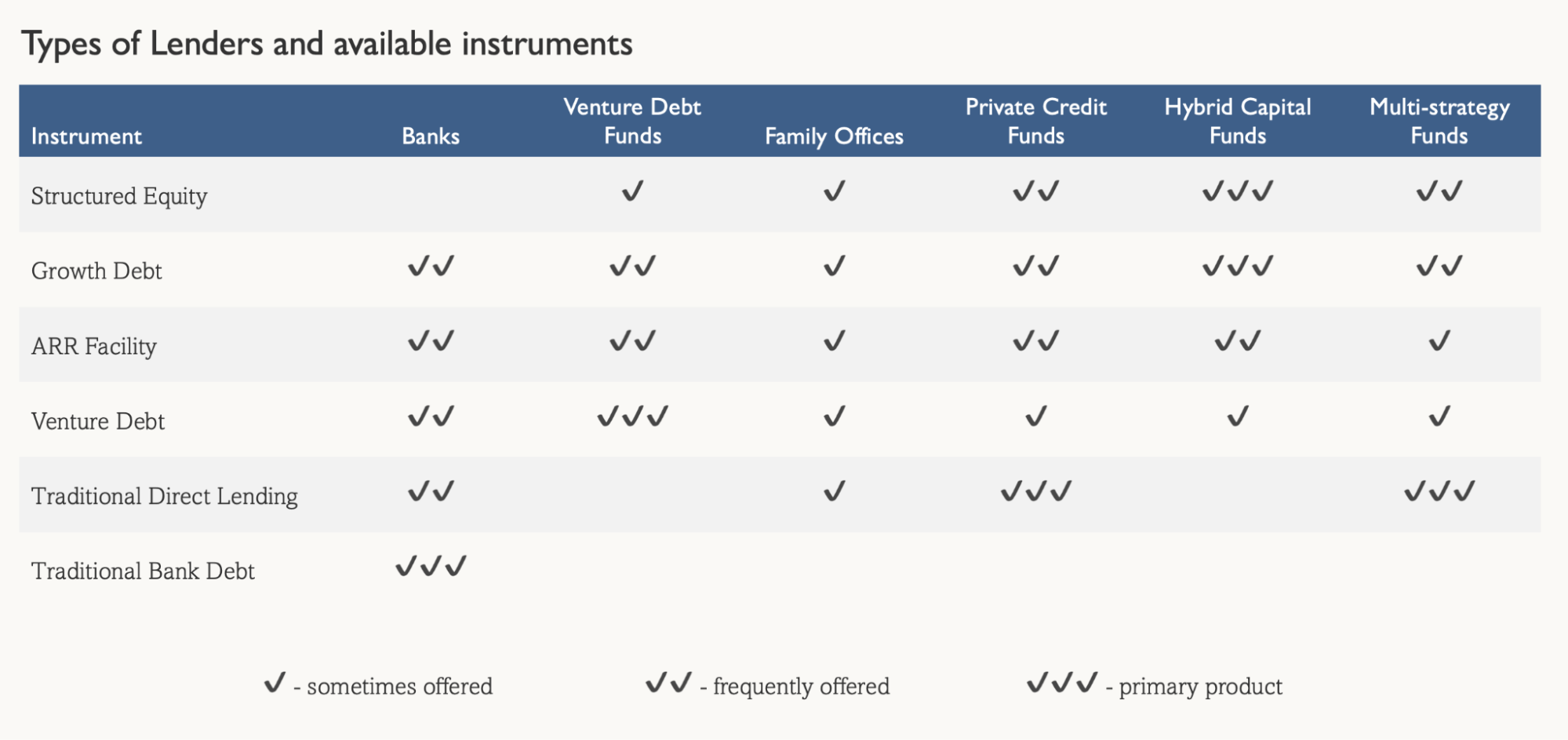

3. Who Are the Players

It's easy to assume that only a handful of institutions offer debt to AI Roll-ups. In reality, the market is large and complex, with a wide range of lenders and solutions available.

Your chances of securing the right kind of debt improve dramatically when you target the right kind of lender - one that matches your company's stage, scale, and risk profile.

The table below outlines the key categories of debt providers and the typical structures they offer.

4. What Lenders Really Look For (Hint: It's Not Like Applying for a Mortgage)

Raising debt for an AI Roll-up isn't a box-ticking exercise. Lenders evaluate your business far more holistically than a traditional bank would for a mortgage. They're underwriting not just your assets, but your strategy, execution capability, and discipline.

Below are the key areas lenders focus on - and what you should be ready to present when approaching them.

1. Acquisition Strategy

Lenders want to understand how disciplined and data-driven your acquisition approach is. Expect questions around:

- How you identify and evaluate targets - from both tech and financial standpoints.

- Typical target characteristics (revenue, growth, margins, etc.).

- The size of your target universe ("TAM") and the depth of your pipeline.

- Your acquisition multiples and valuation methodology.

- Deal structures - including earn-outs, deferred payments, or other performance-linked terms.

2. Post-close Strategy

Debt providers look for clear, repeatable value-creation levers once acquisitions close. Be ready to articulate:

- Your integration plan and how you operationalize synergies.

- The value-creation model (efficiency gains, revenue expansion, cost optimization), ideally backed by a proven track record.

3. Clear Operating Model ("OpMod")

A transparent and credible operating model is non-negotiable. Lenders expect:

- Historical financials (including pre-acquisition data for each asset).

- A detailed 5-year forecast with key assumptions.

- Visibility into expected HQ costs, hiring plans, and R&D investments.

4. Full M&A Pipeline

You'll need to show depth and structure in your pipeline. Lenders will want:

- A ranked list of targets by stage (LOI, diligence, etc.) or likelihood of close.

- Key financial metrics for each - revenue, EBITDA, and margin profile.

5. Proven AI-led EBITDA Uplift

For lenders to underwrite AI uplifts, just having a plan on paper is insufficient. Lenders would apply a haircut to your projections, or even completely disregard them unless:

- The uplift is repeatable across multiple acquired assets,

- It shows up in actual margin changes inside the P&L, or

- It is validated via design partners with real cash impact.

6. Team Background and Equity Sponsors

Ultimately, lenders are backing people as much as plans. They'll assess:

- The team's experience and execution record within the target vertical.

- The quality and depth of your equity sponsors (do they understand the strategy, are they credible).

In short: lenders will conduct due diligence on both your plan and your ability to execute it. Demonstrating clarity, repeatability, and alignment across your acquisition, operating, and financing strategies is what earns confidence - and ultimately, better terms.

5. Key Elements to Consider When Choosing a Lender (Hint: It's Not Just the Interest Rate)

The right lender should fit your roll-up strategy, your risk appetite, and your growth ambitions. Think about the decision around three dimensions:

1. Your Approach to the AI Roll-up Strategy

Different strategies imply different debt partners.

- A high-velocity roll-up with heavy HQ investments (lots of acquisitions, large equity raises, higher product/tech spend) needs a lender comfortable with speed, volatility, and future upside.

- A PE-style buy-and-build (steady, cash-flow-driven, more debt-heavy) needs a lender oriented toward discipline and predictability.

Choose a partner who best understands and supports your operating model.

2. Your Sensitivity to Key Terms

Beyond the interest rate, pay attention to the trade-offs between equity dilution, facility size, advance rate, covenants, and repayment terms. These elements shape both your flexibility and cash flow.

3. Lender-fit and Scalability

Lender-fit is very important. The best lenders scale with you, increasing commitment size as your business grows and transitioning you toward more traditional direct lending structures over time. Lenders are strategic partners, so choose them the way you'd choose an equity investor. The right partner won't just provide capital; they'll understand your acquisition rhythm, share your conviction in the thesis, and support your next phase of growth.

"Sometimes, having a lender who'll pick up the phone and work with you when things go sideways is worth more than shaving a point off your interest rate."

There are many unknown-unknowns in the journey, and it is generally sound advice to optimize for flexibility rather than cost when choosing a debt partner.

6. Debt Capacity Benchmarks

Most founders anchor on Debt-to-EBITDA when thinking about leverage. It's a useful headline metric - but for AI Roll-ups, it is only one of several constraints, and rarely the binding one.

Think of it this way: Debt-to-EBITDA tells you the theoretical maximum you can borrow. But in practice, interest coverage, liquidity minimums, and integration cash burn are what actually limit how much debt you can comfortably carry.

Below is a practical framework for estimating how much debt your AI Roll-up can support today, and what increases your capacity over time.

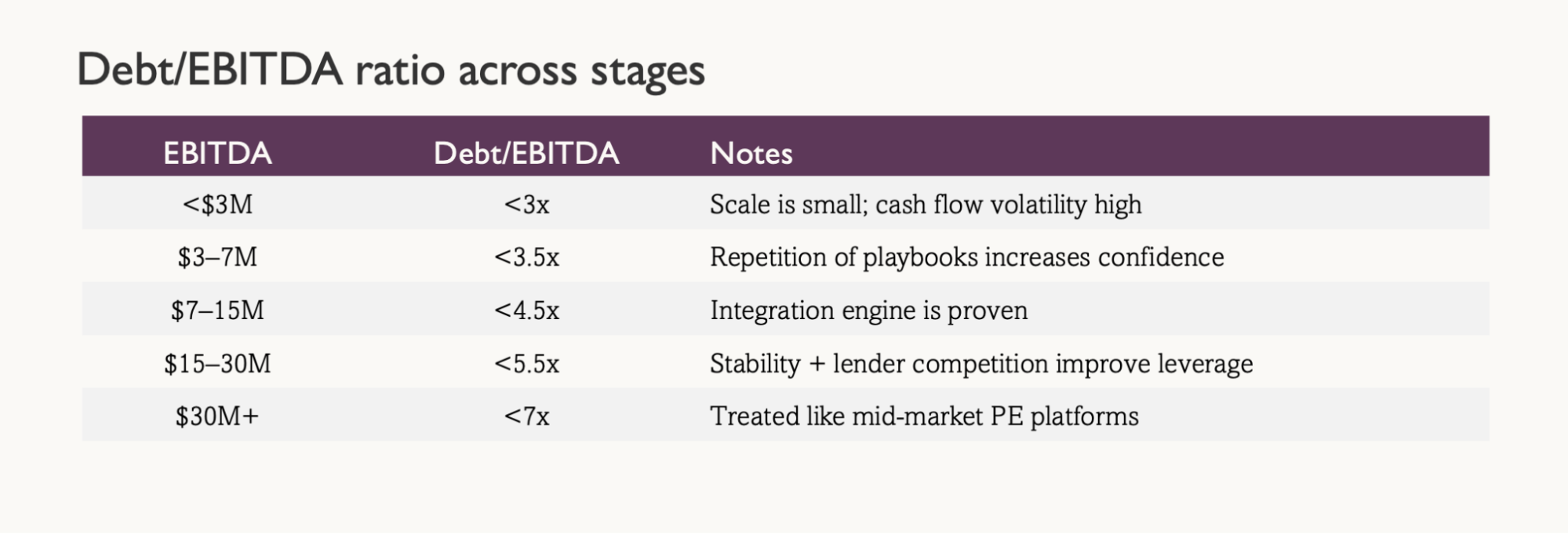

1. Leverage Benchmarks by EBITDA Scale

Debt facilities can be normally structured on 4 different parameters: (1) ARR, (2) Enterprise Value / Total Equity Raised, (3) Asset-level EBITDA, (4) Group EBITDA. For AI Roll-ups, the most common basis is Asset-level of Group EBITDA. The figures below are typical maximum Debt/EBITDA limits across venture debt, growth debt, and private credit funds.

Note 1: While the figures above are broadly true, there are always exceptions. Linus mentions he has even seen cases of 6x Debt/EBITDA at <$7m EBITDA levels.

Note 2: While the above are the theoretical maximum limits, they are not necessarily the recommended Debt/EBITDA levels. Excessive debt could quickly lead to a negative financial spiral, and founders must be prudent about the fact that leverage enables the business plan, without jeopardizing it.

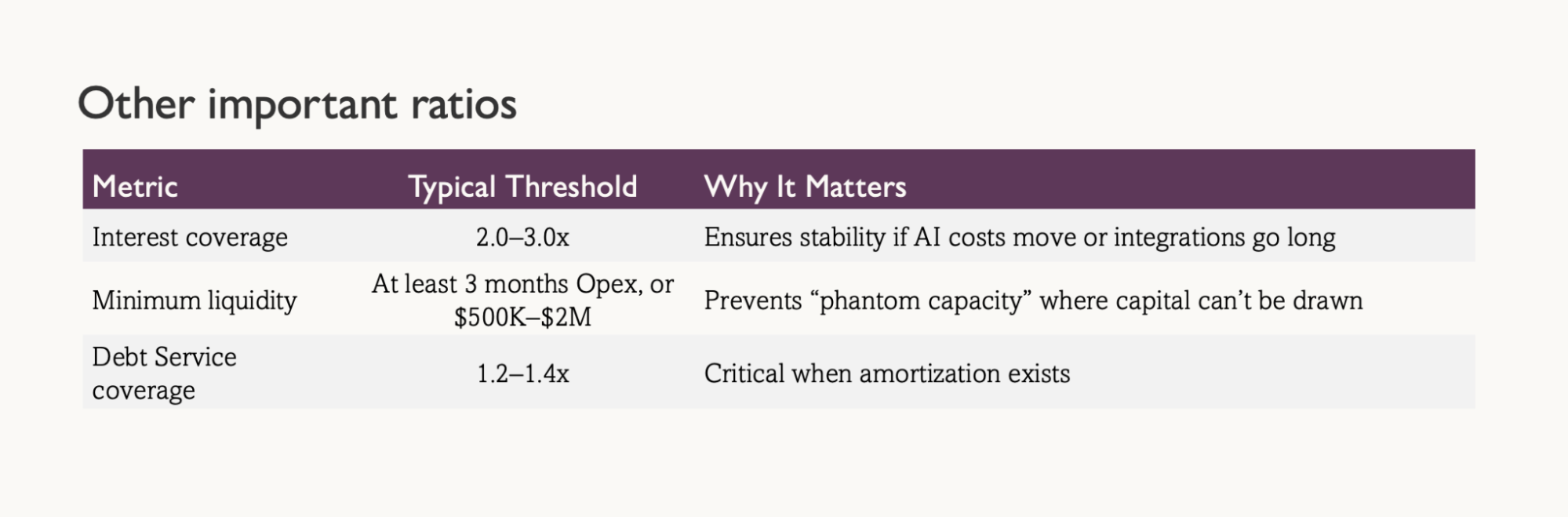

2. Interest Coverage & Liquidity - The True Constraints

Most AI Roll-ups hit debt limits because of interest burden, liquidity minimums, and integration cash burn - not leverage.

For many AI Roll-ups, interest coverage is the actual binding constraint. Minimum liquidity constraints are most relevant for businesses that are still not profitable at a group level, but leverage would sit on ARR or Asset-level EBITDA.

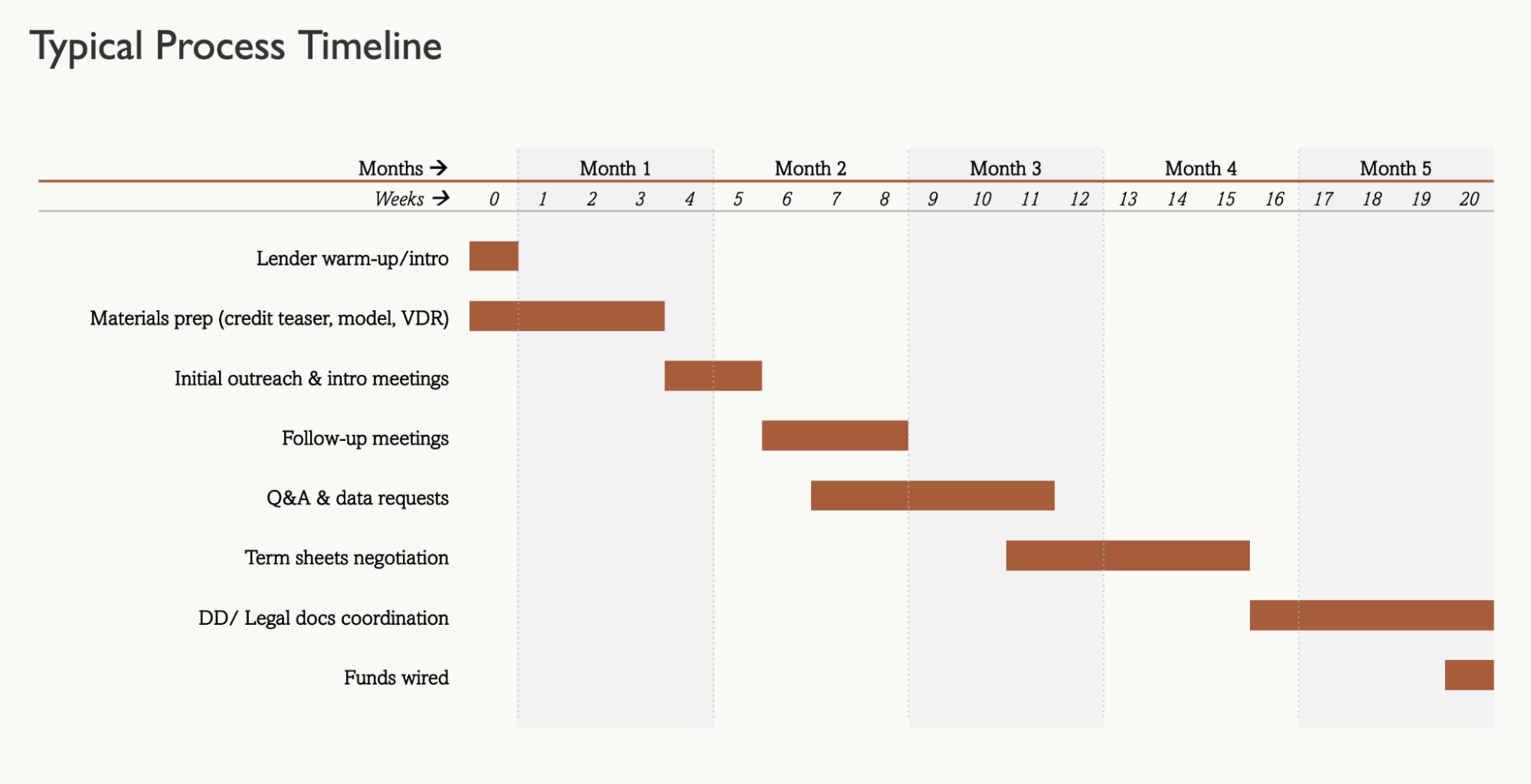

7. Timeline & Process

This is one of the most common questions Linus gets asked. The chart below outlines the typical process and indicative timelines for a debt raise.

While timelines can vary based on deal complexity and lender responsiveness, four to five months is a reasonable estimate for the full process from start to finish. However, in exceptional cases an end-to-end process could be run in as little as two months.

A few things can help you get the best outcome in the shortest time:

- Clean, well-organized data: having your financials, acquisition pipeline, and operating metrics in order speeds up the preparation of lender-ready materials.

- A competitive process: engaging multiple lenders early allows you to use initial term sheets to both accelerate discussions and negotiate stronger terms.

8. The Real Price-tag of a Debt Raise

Raising debt isn't just about securing approval and signing a term sheet - it also involves a range of fees, advisors, and hidden costs that can add up quickly. Founders often underestimate these when budgeting, so it's worth knowing what to expect upfront.

Lender Fees

Most lenders charge an arrangement or commitment fee, typically 1–2% of the facility size, to cover the cost of underwriting and structuring the loan. Some also include monitoring fees for ongoing oversight or exit fees at repayment.

Legal Fees

Legal work for both sides can be significant, especially if multiple entities or jurisdictions are involved. Founders should budget $30K–$100K depending on the complexity of the structure. Lenders often require you to cover their legal costs as well.

Broker or Advisor Fees

If you're working with a credit advisor or debt broker, expect a success fee (usually 1–2% of the facility amount) once the transaction closes. Some advisors may also charge a small retainer or upfront engagement fee.

Due Diligence and Miscellaneous Costs

These can include third-party diligence reports, accounting verification, or valuation support - typically $10K–$25K in aggregate, depending on lender requirements.

All in, transaction-related costs can range from 2–4% of the facility size, sometimes more for smaller deals or complex structures. Plan for these costs early, so you're not caught off guard during closing. A well-prepared borrower (with clean data, a clear structure, and transparent communication) can often minimize these extras and move faster through the process.

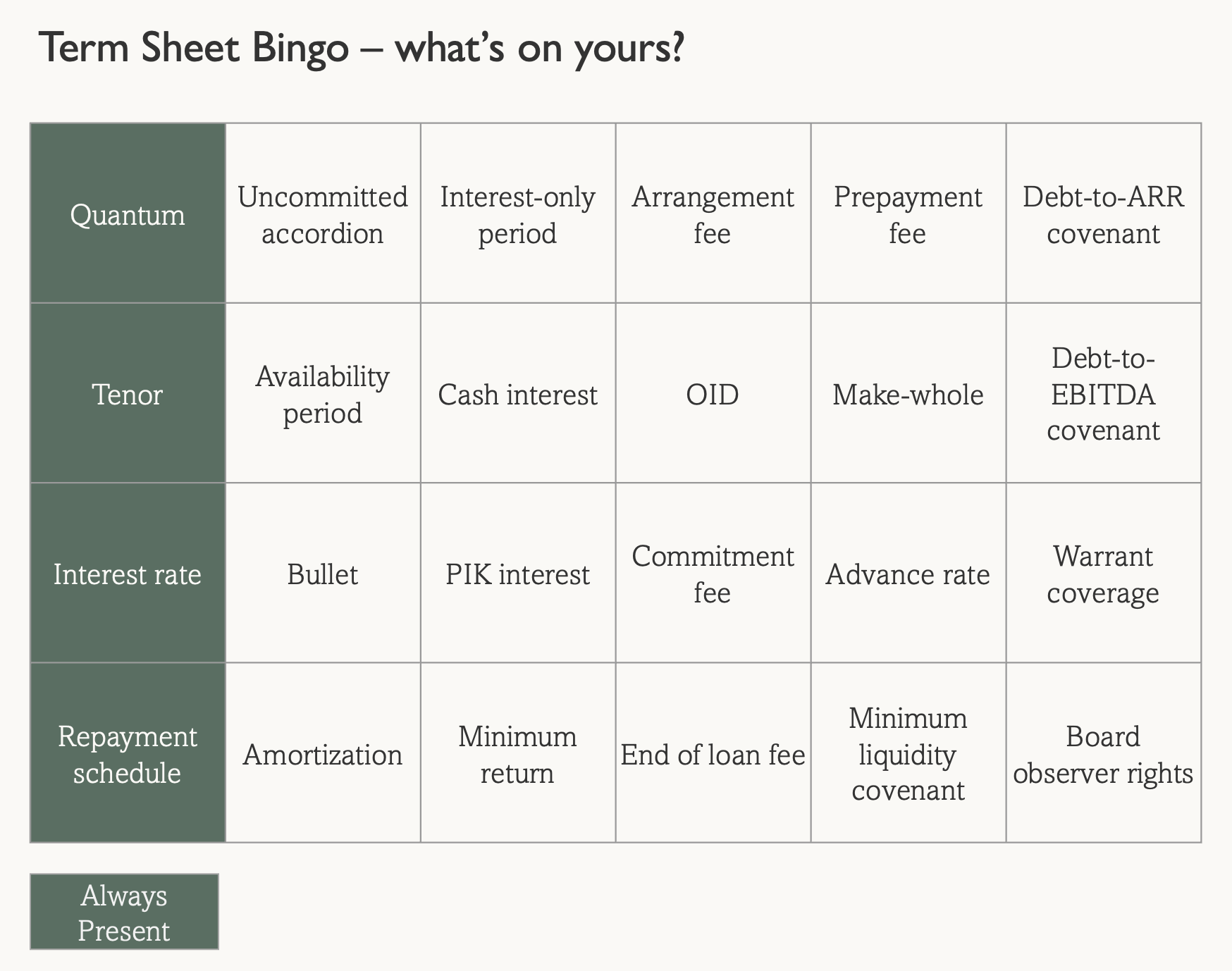

Appendix A: Term Sheet Bingo - What's in My Term Sheet?

While we've already covered the most essential terms in Section 1, the world of lending has evolved into a maze of clauses and conditions that you're bound to encounter at some point. Linus likes to call this game "Term Sheet Bingo" - spotting which terms show up in your deal.

Below is a list of additional terms that aren't always included, but are far from rare in debt term sheets for AI Roll-ups.

And here's a glossary of terms. You can also download it here.

Loan Terms & Structural Features

- Uncommitted Accordion: An optional feature that allows the borrower to increase the total loan commitment in the future, subject to lender approval.

- Availability Period: The time window during which the borrower can draw down funds under the loan agreement.

- Bullet: A structure where the entire principal is repaid in a single lump sum at maturity rather than through installments.

- Amortisation: Repayment of principal in regular installments over the life of the loan, reducing the outstanding balance over time.

Interest & Return Mechanics

- Interest-only Period: A phase during which only interest payments are due, with principal repayment starting later.

- Cash Interest: Interest paid periodically in cash throughout the loan term.

- PIK Interest: Interest that accrues and is added to the loan balance instead of being paid in cash.

- Minimum Return: The lender's guaranteed minimum return on the loan, regardless of early repayment or refinancing.

Fees & Upfront Economics

- Arrangement Fee: A one-time fee paid to the lender or arranger for structuring and setting up the loan.

- OID (Original Issue Discount): A discount on the loan's face value that effectively increases the lender's yield at issuance.

- Commitment Fee: A fee charged on the undrawn portion of a committed facility, compensating the lender for holding capital available.

- End of Loan Fee: A fee payable at the loan's maturity, often used in venture or growth debt to boost lender returns.

Prepayment & Exit Terms

- Prepayment Fee: A charge applied if the borrower repays the loan before maturity, protecting the lender's expected return.

- Make-whole: A clause ensuring the lender receives the full expected interest if the loan is repaid early.

- Advance Rate: The percentage of the underlying collateral value that the lender is willing to lend against.

Covenants & Controls

- Debt-to-ARR Covenant: A ratio limiting total debt relative to Annual Recurring Revenue, used in SaaS or subscription models.

- Debt-to-EBITDA Covenant: A leverage covenant limiting total debt relative to EBITDA, ensuring manageable debt levels.

- Minimum Liquidity Covenant: A requirement to maintain a specified minimum cash or liquidity buffer during the loan term.

- Board Observer Rights: Rights allowing the lender to attend board meetings as a non-voting observer, enhancing visibility into company performance.

Other Economic & Structural Provisions

- Warrant Coverage: The percentage of company equity offered to the lender as warrants, serving as an equity kicker.

Appendix B: Watchouts and Horror Stories

I hope the prior sections have given you the tools to approach your debt raise with confidence. Yet even with great preparation, founders can encounter blind spots that only show up once the process is underway. Here are some real-world horror stories to help you anticipate (and dodge) the pitfalls.

The Phantom Liquidity Trap

A founder secured a $5M debt facility, only to discover that minimum liquidity covenants meant they could actually deploy just $3M. The remaining "dry powder" sat unusable on the balance sheet, while interest and fees still accrued. Always model true usable proceeds, not just the headline facility size.

Covenant Handcuffs During Acquisition Season

Aggressive or poorly negotiated covenants can grind your M&A engine to a halt. Some operators found that every new deal required lender approval - or worse, a bridge equity round to keep ratios in check. Debt meant to accelerate acquisitions instead delayed them at the worst possible time.

Raising Debt at the Wrong Level (TopCo vs. AssetCo)

A common pitfall is taking debt at the wrong entity level and discovering after the fact that lenders treat cash flows, collateral, and covenants differently. Operators raised at TopCo only to learn it offered no credit uplift, or at asset level where cross-collateralization created unintended contagion risk. Structure matters as much as pricing.

The Floating Rate Shock

Variable-rate facilities looked cheap - until rates spiked mid-cycle. Overnight, interest payments doubled and wiped out cash flow earmarked for acquisitions or integration. Some platforms had to pause roll-ups entirely just to stay covenant-compliant.

"Deploy It or Lose It" Facilities

Certain lenders include ticking clocks on drawdowns. Founders raced to deploy capital into suboptimal acquisitions simply to avoid losing access to the facility. The result: worse deals, higher integration risk, and a debt structure that pressures speed over quality.

Flexibility Lost to a Rigid Annual Plan

Operators built a smarter, more profitable plan mid-year - but their debt agreement was tied tightly to the original forecast. Deviating would trigger covenant breaches, so teams were forced to follow an outdated strategy despite knowing better. Debt turned learning agility into liability.

The Minor Breach That Became a Major Crisis

One founder slipped a small, technical covenant - something they assumed would result in a simple waiver. Instead, the lender panicked, froze the facility, and swept cash from operating accounts. The business spent months negotiating its way out of crisis mode over a spreadsheet footnote.

Appendix C: FAQs

Q1: I am planning to have my TopCo in Geo X because of easier access to equity capital and public markets, but want to acquire assets in Geo Y. Is that a challenge from a debt fundraise perspective?

A: No. International structures are common. Lenders simply prefer to place debt closer to the underlying cashflows, so the facility will likely be raised at the MidCo/AcquiCo in Geo Y. This is standard and not a disadvantage.

Q2: What legal structure do lenders typically expect?

A: Most lenders prefer to lend at the AcquiCo/MidCo level so they have direct access to cashflows. They expect a clean separation between operating entities and the TopCo/HQ.

Q3: I hear lenders have stringent reporting requirements. What should I expect? Do I need a senior finance hire early?

A: Reporting is clearly defined in the loan documents but generally overlaps with what equity investors require. A senior finance hire isn't strictly necessary as long as monthly financials and core data are reliable.

Q4: How are earn-outs treated when calculating leverage ratios?

A: Treatment varies slightly by lender. Small earn-outs may be discounted, especially if funded from the acquired business's cashflows. Larger deferred consideration is typically included as debt for leverage and covenant calculations.

Q5: How do AI-driven EBITDA uplifts get treated by lenders during decision-making?

A: Lenders usually apply a haircut to projected AI-driven improvements unless they have already been demonstrated across acquisitions. Proven uplift either in acquired companies or design partners may be partially credited; unproven uplift is generally excluded.

Q6: Is it a problem if my acquisitions vary in size, margin, or business model?

A: Not necessarily. Lenders mainly care about predictability of combined cashflows and consistency of your integration process.

Q7: Can debt proceeds be used to fund AI platform development?

A: Sometimes. Smaller or more flexible lenders may allow it if the spend is tied to integration or operational efficiency. Larger lenders generally prefer debt to fund acquisitions and working capital, not long-term R&D.

Q8: Do lenders require personal guarantees?

A: Not for institutional lenders. Personal guarantees are more common only in very small or non-bank facilities.

Q9: How flexible are lenders when it comes to add-on acquisitions after the facility is in place?

A: Most lenders allow add-ons within predefined parameters. Only large or unusual acquisitions require explicit approval.

Q10: Do lenders care who my equity investors are?

A: Yes. Credible, long-term equity sponsors who have a clear understanding of the thesis give lenders confidence in governance and future funding. This can materially improve terms.

Q11: Are ARR-based lenders relevant for AI Roll-ups?

A: They can be early on if you have strong recurring revenue. But they're typically a bridging solution until you scale into EBITDA-based private credit.

Q12: Can I refinance early if better terms become available?

A: Usually yes, though prepayment fees may apply. As the roll-up scales, refinancing into larger and cheaper facilities is common.

Q13: What happens if I miss a covenant?

A: Minor breaches are usually handled through waivers, but meaningful or repeated breaches can freeze drawdowns or trigger renegotiation. Transparent communication is critical.

Q14: Will lenders penalize me for rapid acquisition velocity?

A: Not if your integration playbook is consistent and performance remains stable. Some lenders actually prefer higher velocity if execution quality is clear.

About the Authors

Linus Eriksson Noren is the Founder of TechCredit Partners, a London-based debt advisory firm helping tech and high-growth companies structure the right debt facilities from seed to IPO. With a network of 400+ lenders and investors across four continents, Linus and his team have become a go-to partner for founders navigating the complexity of debt capital markets.

Sahil Patwa is a General Partner at Tenet, Europe's first inception-stage investment firm dedicated to AI-Powered Roll-Outs (AIPRO). He is also the creator of AI Roll-up Nexus, a public resource hub for AI Roll-up founders and investors.